Share this post

No items found.

I was discussing Stephanie Palazzolo's article "Anthropic Releases New AI, Hurting Financial Services Stocks" with my Sr. Backend Eng Shelby and he had a really good POV on the hammering SaaS companies have received in the public markets this week:

"We're entering a world where the "Build vs. Buy" equation has shifted. And we've seen this movie before."

Shelby partnered with Storytell to write this piece based on that observation:

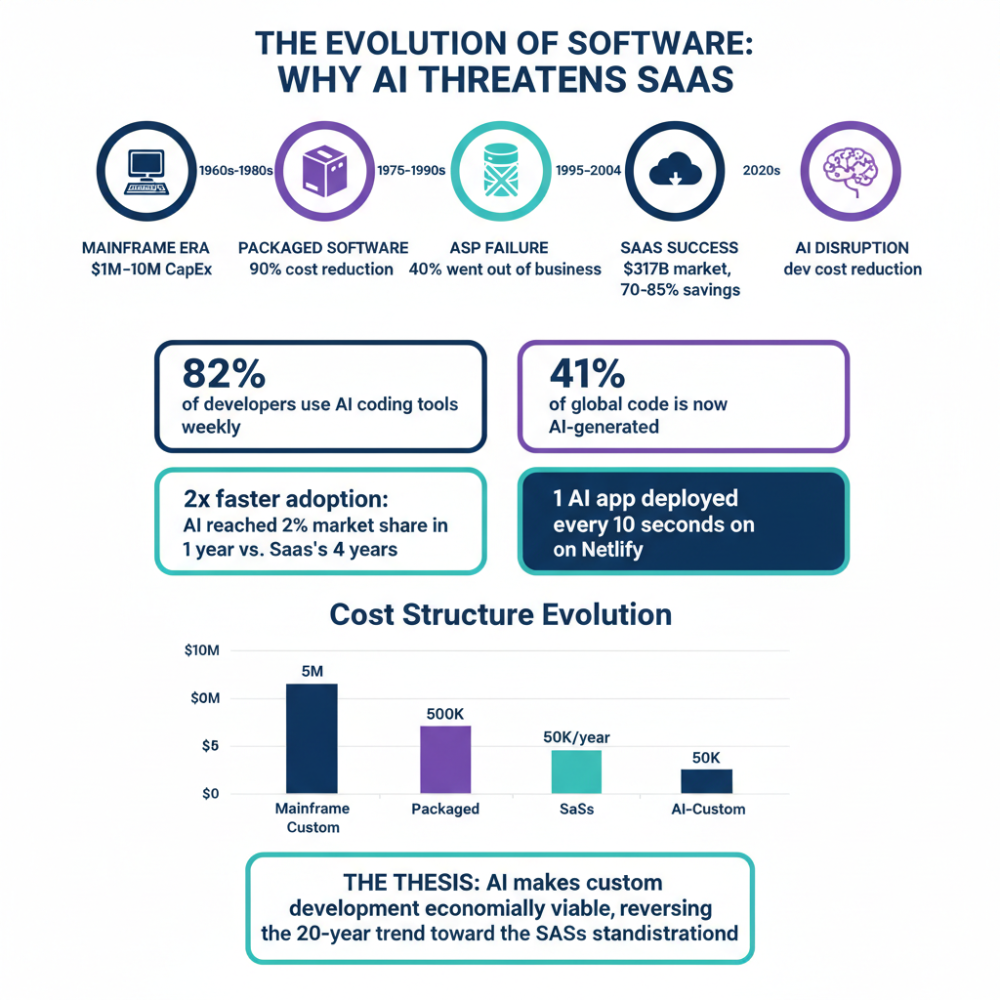

The software industry has undergone four major paradigm shifts, each driven by technological advances that made software dramatically more accessible and cost-effective. Understanding this pattern reveals why AI-generated code represents an existential threat to traditional SaaS business models.

When IBM announced the System/360 in 1964, it revolutionized commercial computing by establishing a standardized architecture. By the time the AS/400 launched in August 1988, IBM had created an ecosystem with 111,000 installations by 1990, growing to 500,000 by 1997.

Economic Structure:

Before the 1969 DOJ settlement forced IBM to unbundle software from hardware, virtually all software was custom-written. Each organization's business processes were considered unique enough to require bespoke solutions. The global packaged software market barely existed—less than $3 billion globally in 1981.

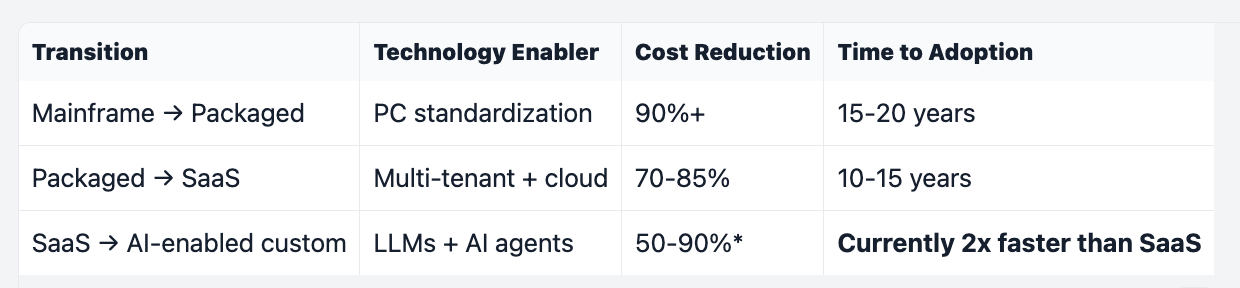

What triggered the transition: Standardization became economically viable as businesses recognized that many processes (accounting, payroll, inventory) followed similar patterns across organizations.

The emergence of packaged software fundamentally altered the economics of software consumption. Key milestones:

Economic Revolution:

Organizations sacrificed customization for cost efficiency. The decision framework emerged: standardize commodity functions (accounting, word processing) and customize only for competitive differentiation. By the 1990s, software product revenue had overtaken services revenue, marking the ascendancy of the one-to-many model.

What triggered the next transition: The internet promised to eliminate even the residual friction of physical distribution and on-premises installation.

Mid-1990s Application Service Providers (ASPs) attempted to deliver software over the internet, forming the ASP Industry Consortium in 1999 with players like HP, SAP, and Qwest. Market projections were euphoric—IDC estimated $7.8B by 2004, Gartner predicted $25.3B.

Reality: 40% of ASPs active in 2001 were out of business by 2004.

The ASP model attempted to solve the right problem (reduce capital expenditure, simplify IT) with the wrong architecture at the wrong time.

What triggered the SaaS revolution: Multi-tenant architecture + cloud computing infrastructure + ubiquitous broadband fundamentally changed the unit economics.

Salesforce, founded in February 1999, launched in 2000 with its famous "No Software" campaign. The company went public in June 2004, raising $110 million. By 2025, Salesforce serves 150,000+ customers with ~$35B+ in annual revenue.

Economic Transformation:

By 2025, 94% of enterprises use cloud services, and SaaS represents ~$195B of the top 500 U.S. software firms' revenue.

Even during SaaS's dominance, custom development never disappeared. Organizations continued building custom software when:

However, the economics remained challenging:

This created the classic "build vs. buy" framework: buy standardized SaaS for commodity functions, build custom only for strategic differentiation.

What is triggering the next transition: AI is collapsing the cost, time, and skill barriers to custom software development.

Adoption Timeline:

Market Growth:

AI adoption is 2x faster than SaaS adoption was.

Perhaps most significantly, AI is enabling non-engineers to build functional applications. One documented example: a non-engineer built a functional app "half a bottle of wine later" that replicated a multi-million dollar company's functionality.

Current deployment velocity: 1 new AI-built app is deployed on Netlify every 10 seconds.

Every software delivery paradigm has been disrupted by a successor that solved the same problems more efficiently and more cheaply:

AI is reducing custom development costs by 50-90%, making custom competitive with SaaS subscription costs at scale.

Traditional Economics (Pre-AI):

AI-Enabled Economics (Current):

When custom software becomes economically competitive with SaaS subscriptions, the primary reason to tolerate standardized solutions disappears.

Seat-based pricing model threatened:

Salesforce's response signals the threat: The company launched "Agentforce" autonomous agents in 2024, explicitly recognizing that AI agents will replace traditional per-seat licensing models.

Industry Analysis:

Market Bifurcation:

Infrastructure Software (Winners):

Application SaaS (Vulnerable):

AI model costs are collapsing:

SaaS Era Logic: Standardization = economies of scale = lower cost

AI Era Logic: AI enables "mass customization" at standardized costs

The 20-year trend toward standardization is reversing because AI makes customization economically viable again.

Characteristics:

Examples: Single-purpose tools for scheduling, form-building, simple CRMs, basic project management

Why vulnerable: An AI agent can replicate these features in hours or days, customized to exact needs, at a fraction of the subscription cost.

Characteristics:

Response required: Integrate AI deeply, shift pricing from seats to outcomes, build stronger data network effects

Characteristics:

Why defensible: Switching costs are prohibitive, data moats are defensible, and ecosystem effects create lock-in.

The software industry's history shows a clear pattern: technological paradigms that dramatically reduce cost and increase accessibility always disrupt incumbent delivery models.

The thesis is not speculative—it is already happening:

The strategic question for SaaS companies is not WHETHER disruption will occur, but HOW to respond:

The companies that built SaaS empires by standardizing software delivery now face the same disruption that mainframe vendors and packaged software companies faced before them. The standardization that created their competitive advantage is becoming their vulnerability in an era where AI makes customization economically viable.

History doesn't repeat, but it rhymes. And the pattern is clear: the next paradigm always wins by making the expensive and complex become cheap and accessible. AI is doing exactly that to custom software development, and SaaS sits directly in the path of that disruption.